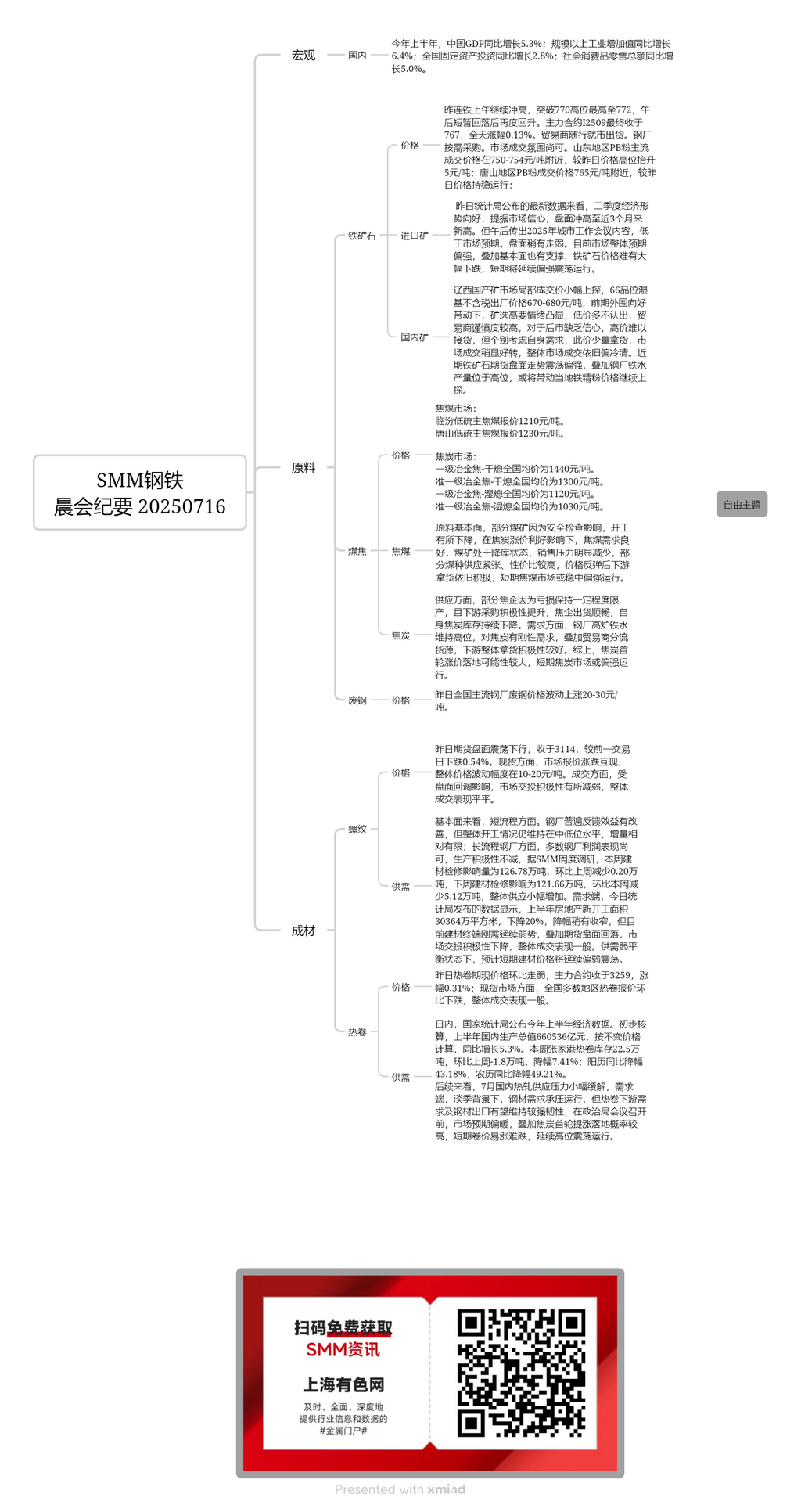

Domestic ore:

In the Liaoxi domestic ore market, local transaction prices saw a slight increase. The ex-factory price (wet basis, excluding tax) for ore with a 66% grade was 670-680 yuan/mt. Driven by the positive external environment, ore suppliers were more inclined to hold out for higher prices and were reluctant to sell at lower prices. Traders were cautious and lacked confidence in the future market, making it difficult for them to purchase at high prices. However, some traders, considering their own needs, purchased small quantities at these prices, leading to a slight improvement in market transactions. Overall, the market remained sluggish. Recently, the iron ore futures market has shown a fluctuating upward trend, coupled with the high pig iron production at steel mills, which may drive the local iron ore concentrate prices to continue rising.

Imported ore:

Yesterday, the DCE iron ore futures continued to rise in the morning, breaking through the 770 level and reaching a high of 772, before pulling back briefly in the afternoon and then rebounding again. The most-traded contract I2509 eventually closed at 767, with a daily increase of 0.13%. Traders sold according to market conditions, and steel mills purchased as needed. The market transaction atmosphere was moderate. In the Shandong region, the mainstream transaction price of PB fines was around 750-754 yuan/mt, up 5 yuan/mt from the previous day's high price. In the Tangshan region, the transaction price of PB fines was around 765 yuan/mt, remaining stable compared to the previous day. According to the latest data released by the National Bureau of Statistics today, the economic situation in Q2 was positive, boosting market confidence. The futures market surged to a new high in nearly three months. However, in the afternoon, news emerged about the content of the 2025 Urban Work Conference, which was lower than market expectations, causing the futures market to weaken slightly. Currently, the overall market expectation is strong, and the fundamentals also provide support. It is difficult for iron ore prices to fall sharply in the short term, and they will continue to hold up well in the short term.

Coking coal:

The price of low-sulphur coking coal in Linfen is 1,210 yuan/mt. The price of low-sulphur coking coal in Tangshan is 1,230 yuan/mt.

On the cost side, coal mines are maintaining stable production, and supply is temporarily stable. Downstream coking and steel enterprises are actively purchasing coking coal. Coal mine coking coal inventories have dropped to a medium-low level, and online auction market transactions have performed well, with participants actively bidding. The overall trading atmosphere in the market is good, and there is still upside room for coking coal prices in the short term.

Coke:

The nationwide average price of first-grade metallurgical coke (dry quenching) is 1,440 yuan/mt. The nationwide average price of quasi-first-grade metallurgical coke (dry quenching) is 1,300 yuan/mt. The nationwide average price of first-grade metallurgical coke (wet quenching) is 1,120 yuan/mt. The nationwide average price of quasi-first-grade metallurgical coke (wet quenching) is 1,030 yuan/mt.

In terms of supply, coking enterprises have recently expanded their losses, and some have voluntarily implemented production restrictions, leading to a tightening of coke supply. In terms of demand, the current production restriction notice in Shanxi has not yet been formalized, and pig iron production at steel mills remains at a high level, with restocking needs. On the news front, mainstream steel mills in Hebei and Shandong intend to postpone the first round of coke price increases to this Friday (July 18th), accepting an increase of 50-55 yuan/mt. The previous coking enterprises' proposed increases of 70-75 yuan/mt and 90-95 yuan/mt are still under discussion. In summary, coking enterprises have good shipment conditions, coupled with strong cost support. The coke market may hold up well in the short term, and a consensus has been reached on the first round of coke price increases.

Rebar:

Yesterday, the futures market fluctuated, with a slight increase in the afternoon, closing at 3,138, up 0.16% from the previous trading day. In the spot market, most market quotes remained stable, with some markets experiencing secret price reductions for shipments. Overall, price fluctuations were relatively small. In terms of transactions, compared to last week, there was a slight pullback, with general purchasing for immediate needs.

From the fundamental perspective, in the short-process production, as spot prices rise, steel mills' profitability has slightly improved, but most are still operating at a loss. It is expected that the operating rate will remain at a moderately low level in the short term, with no significant increase. In the long-process production, most steel mills' profits are moderate, and their production enthusiasm remains high, with little change in overall supply. On the demand side, the current hot and rainy weather continues, limiting the progress of construction projects at construction sites. The actual demand for purchases is weak, and overall transactions rely more on sentiment-driven factors. Overall, in an environment of stable supply and weak demand, the weak reality may drag down the height of spot price increases. It is expected that prices will continue to be in the doldrums today.

HRC:

Yesterday, HRC futures and spot prices held up well, with the most-traded contract closing at 3276, up 0.09%. In the spot market, most markets across the country maintained stable quotes, with overall transaction performance being moderate. In terms of data, according to SMM shipping data, during this week, China's steel port departures from main ports reached 3.1363 million mt, up 28% WoW, indicating strong export performance.

Looking ahead, on the supply side, according to the latest tracking by SMM, the planned daily production of hot-rolled commodity materials for 39 mainstream steel mills producing HRC in July is 464,200 mt, a decrease of 2.72% compared to the actual daily average production of hot-rolled commodity materials in June. The planned daily average production of hot-rolled materials for domestic steel mills in July decreased MoM compared to the actual production in June. On the demand side, amid the off-season, with frequent hot and rainy weather, the overall demand for steel is under pressure. However, the downstream demand for HRC and steel exports are expected to maintain strong resilience. In addition, on the macro side, amid the dual policy "warm winds" of "anti-rat race competition" and the Political Bureau meeting, market sentiment has recovered. It is expected that HRC prices will hold up well in the short term. However, the overall pullback in steel demand during the off-season will limit the upside room for HRC prices.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)